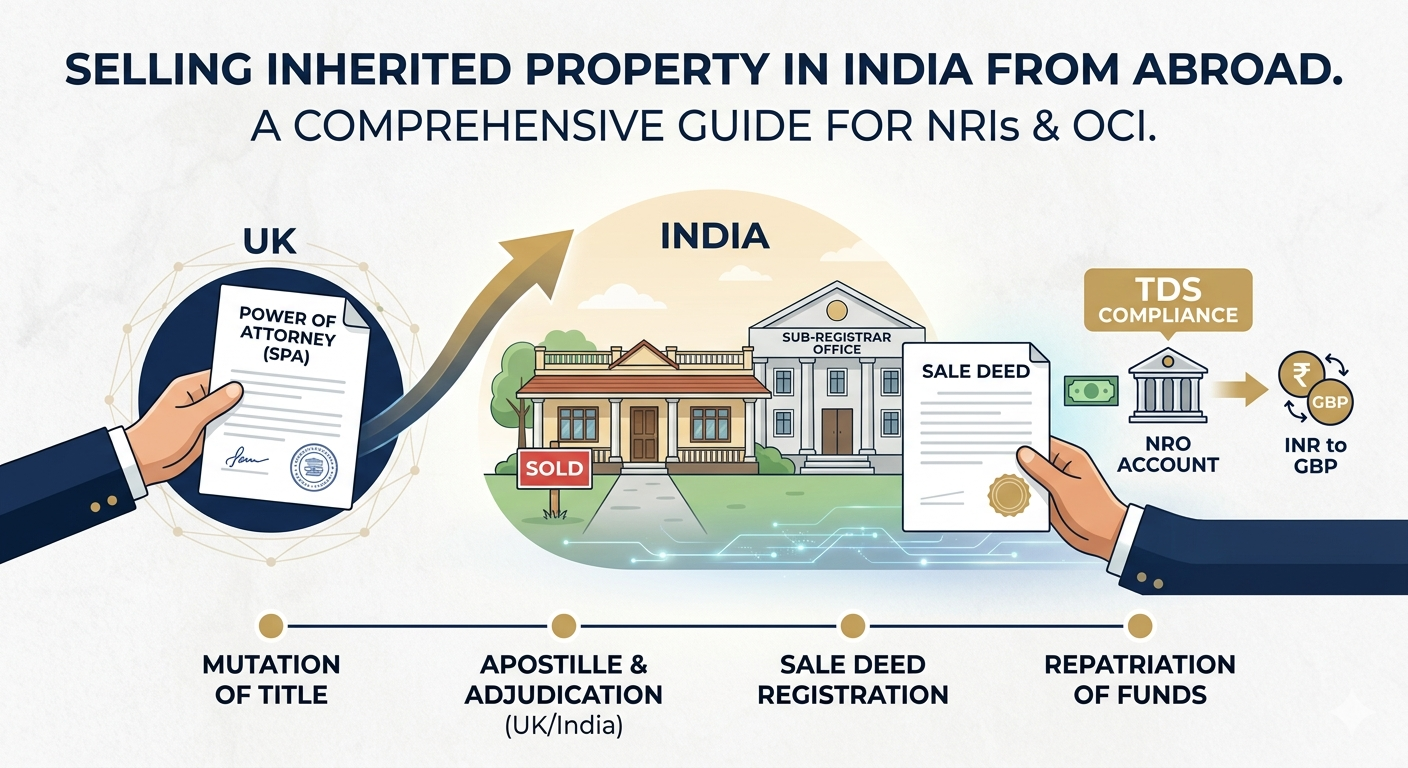

Inheriting property in India while living overseas sounds complicated — and honestly, it can be. But Indian law has a clear, structured path that lets you sell legally and move your money abroad without a single flight home.

Mutation of Title — the non-negotiable first move

You cannot sell a property still registered in a deceased parent’s name. Mutation updates the government’s revenue records so you appear as the current owner. You’ll need the original Death Certificate and a Legal Heir Certificate from a competent court, if the deceased left a registered Will naming you as beneficiary, a Probated Will can substitute the Succession Certificate and considerably speeds up the mutation process.”

GPA vs. SPA — the 2011 Supreme Court ruling you must know

A common and expensive mistake: assuming a General Power of Attorney (GPA) is enough to sell. The Supreme Court shut that door firmly in Suraj Lamp & Industries v. State of Haryana (2011). A GPA cannot legally transfer title of immovable property.

Executing a POA from abroad — the Apostille process

For your foreign-signed SPA to be recognised by Indian sub-registrars, follow this four-step sequence:

Once the original reaches India, your attorney must have it adjudicated (stamped) by the District Collector or Sub-Registrar within 3 months of arrival. Miss that window and you start over.

How the actual transaction works

The buyer in India attends the Sub-Registrar’s office in person to sign the Sale Deed. Your appointed attorney — armed with the valid, stamped SPA — signs on your behalf. The deed is then registered, title transfers, and the transaction is complete. Simple, once the paperwork is right.

Tax compliance & moving your money

The financial side of an NRI property sale is tightly regulated under the Income Tax Act and FEMA. Here is what both sides of the transaction must do.

| Item | Requirement |

|---|---|

| TDS Rate | Buyer deducts at a base rate of 12.5% (effective ~14.95% including cess and surcharge). |

| Lower TDS Certificate | Apply in Form 13 to prevent excess tax being withheld at source. |

| Banking | Sale proceeds must be deposited into the seller’s NRO account first. |

| Repatriation | You can repatriate up to USD 1 million per financial year, supported by Forms 15CA and 15CB from a Chartered Accountant. |

| Buyer’s obligations | Buyer must obtain a TAN and file a TDS return in Form 27Q. |

Conclusion:

Selling inherited property in India while living abroad is genuinely manageable if you follow the sequence: mutate the title first, use an Apostilled SPA (not a GPA), ensure a registered Sale Deed closes the deal, and have your tax affairs in order before proceeds are released.

The process rewards preparation and punishes shortcuts. Engage a property lawyer in India who has experience with NRI transactions — the cost is trivial relative to the value of the asset.